Medigap Plan N

Medigap Plan N is a supplemental policy that saves you on your monthly premium by having you pay for your Medicare Part B deductible, excess charges, and some of your copays for doctor’s office, and emergency room visits.

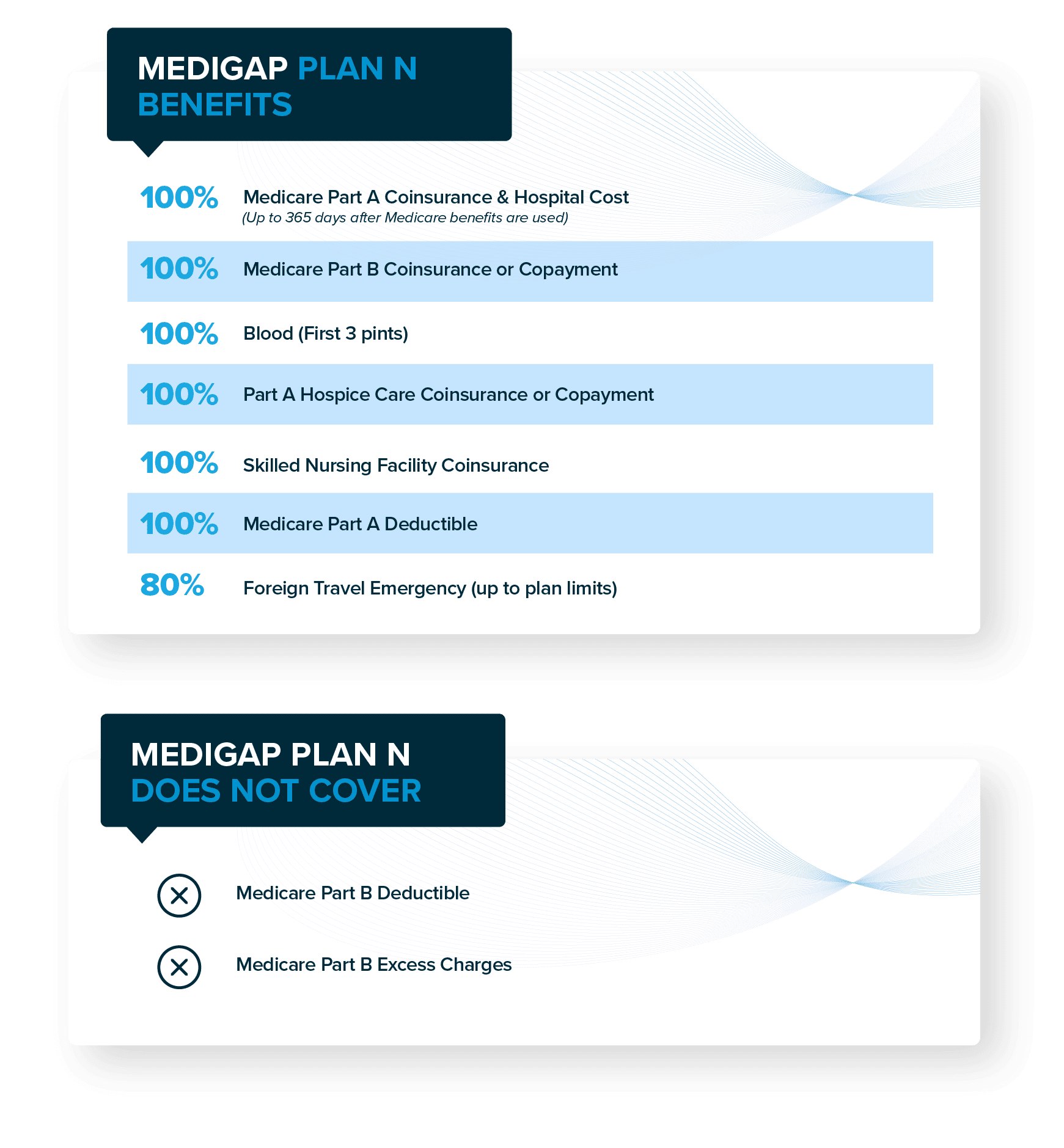

What does Medigap Plan N cover?

Medicare Supplement Insurance Plan N covers:

- Medicare Part A hospital coinsurance and other costs up to an additional 365 days after Original Medicare benefits are used up

- Medicare Part A hospice care coinsurance or copayments

- Medicare Part A deductible

- Medicare Part B coinsurance or copayments*

- First three pints of blood used in a medical procedure

- Skilled nursing facility care coinsurance

- 80% of foreign travel emergency care (up to plan limits)

The only thing you pay for regarding your Medicare Part B coinsurance or copayments is you’ll pay $20 copay for some doctor’s office visits and up to a $50 copay for emergency room visits if you aren’t admitted as an inpatient.

What isn’t covered under Medicare Supplement Plan N?

Plan N does not cover Medicare part B’s deductible or any Part B excess charges. Also, as mentioned, you may have to pay $20 copay for doctor visits and $50 for emergency room visits if you aren’t admitted as an inpatient. This allows for full coverage of a lot of other costs you’d normally be on the hook for while also keeping your monthly premium lower than comprehensive medicare supplement plans.

Medicare Supplement Plan N eligibility

Like any other Medigap plan, you are eligible as long as you are enrolled in Medicare Part A and B.

If you are considering a Medicare Supplement, the best time to purchase one is during Medigap’s open enrollment period. This window begins on the first day of the month that you are age 65 or over and enrolled in Medicare Part B. During this open enrollment, you are usually guaranteed eligible to enroll in any medicare supplement insurance plan even if you have pre-existing health conditions. You will also not be charged a higher premium for any pre-existing health conditions. The only condition is you have to be enrolled in Original Medicare.

However, you are able to apply for a Medicare Supplement plan at any time. If you are interested in having your Medicare cost-sharing at least partially covered, or even fully covered, a licensed Medicare agent at Bobby Brock Insurance can help you find a plan that fits your budget and healthcare needs!