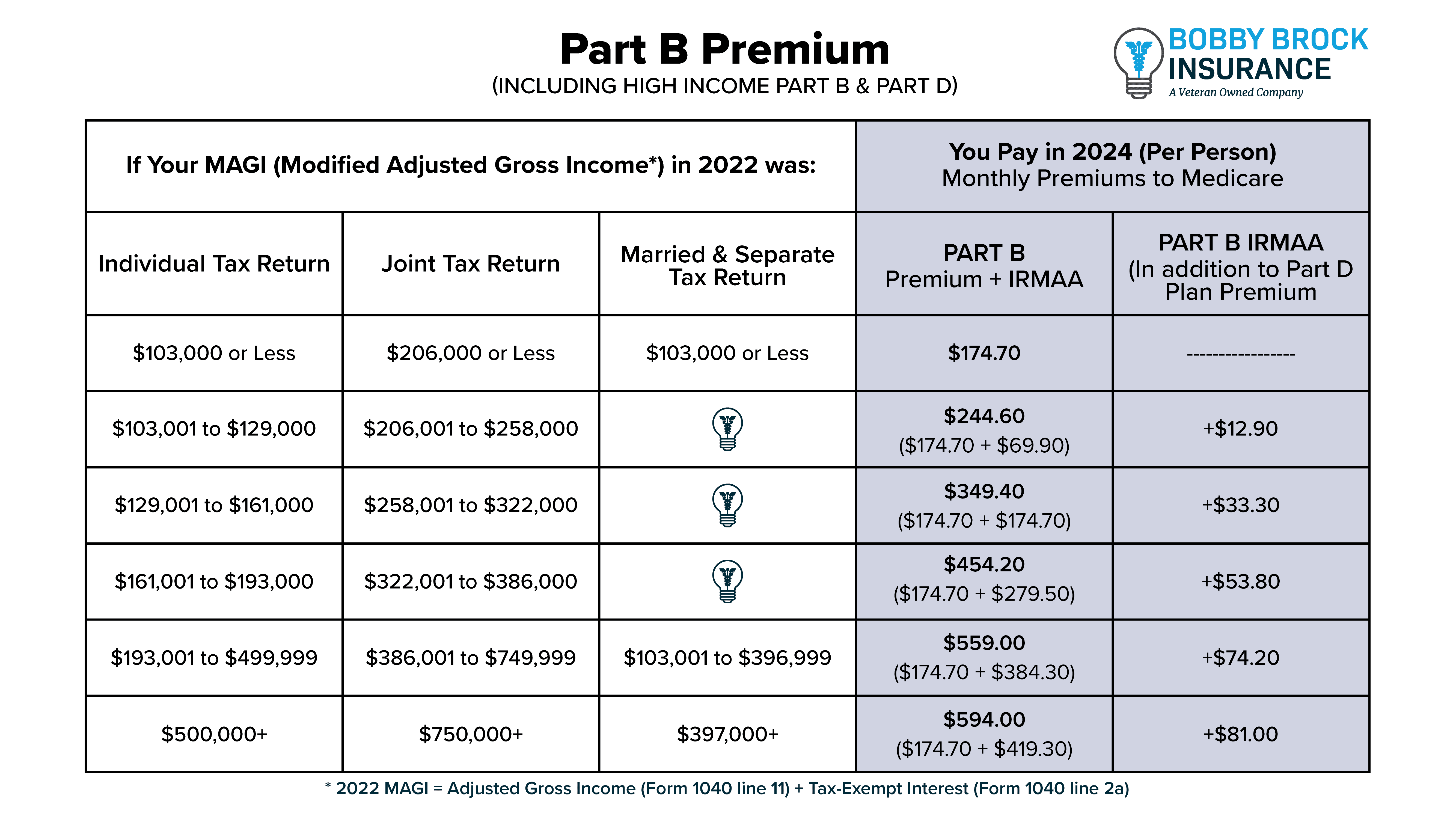

What Is Medicare Part D?

Medicare Part D is a federal prescription drug plan program administered through private insurance companies. Medicare beneficiaries can enroll in a standalone Part D plan to supplement their benefits under Original Medicare, or they can choose to enroll in a Medicare Advantage (Part C) plan that includes prescription drug coverage.

The only way to get prescription coverage is through a Part D plan (or a Medicare Advantage Prescription Drug plan, also known as an MAPD plan). Original Medicare (Parts A and B) does not include coverage for prescriptions that you’d usually get at your local pharmacy. Part D plans require a separate monthly premium and have their own deductibles, copayments, and coinsurance costs.

If you enroll in a Part D plan, you’ll get a separate Part D insurance card that you’ll need to present when you refill your prescriptions.

How Does Medicare Part D Work?

Part D plans are a bit complicated. They work in several phases, each having different costs associated with your prescriptions. Whether you have a standalone Part D plan or have one built into your Medicare Advantage plan, your drug coverage works the same way.

Prescription plans have four phases of coverage.

Phase 1: The Deductible Phase

Each year, the Centers for Medicare and Medicaid Services (CMS) sets a standard deductible for Part D plans. Insurance companies can choose to use this standard amount or set a lower amount. You will remain in the first phase of coverage until your deductible has been met.

The good news is that most plans waive the deductible for the first tier or two of their drug formularies. A drug formulary is the list of prescriptions covered by the plan. The formulary is divided into tiers. Drugs in lower tiers cost less than those in higher tiers. If you are filling a prescription that falls into the first tier of the formulary, it’s likely you won’t have to pay the deductible.

Phase 2: Initial Coverage

Once you’ve met your deductible, you’ll enter the initial phase of coverage. During this time, you pay a copay for each prescription based on the tier it falls into. Tiers are usually defined as follows:

- Tier 1: Preferred generic drugs (least expensive)

- Tier 2: Preferred name-brand drugs

- Tier 3: Non-preferred name-brand drugs

- Tier 4: Speciality drugs (most expensive)

You’ll remain in the initial phase of coverage until you and your plan have spent a certain amount. That amount changes each year, but in 2024, it’s set at $5,030.

Phase 3: The Donut Hole

Here’s where things start to get a little tricky. When you leave the initial coverage phase, you enter the Part D donut hole, also known as the coverage gap. During this time, you’ll pay more for your prescriptions.

Once you and your plan spend $5,030 combined on drugs (including deductible), you’ll pay no more than 25% of the cost for prescription drugs until your out-of-pocket spending is $8,000 in 2024 under the standard drug benefit.

Phase 4: Catastrophic Coverage

Starting January 1, 2024, once your out-of-pocket spending reaches $8,000 (including certain payments made by other people or entities, including Medicare’s Extra Help program, on your behalf), you’ll automatically get “catastrophic coverage.” This means you won’t have to pay a copayment or coinsurance for covered Part D drugs for the rest of the calendar year.

The Medicare Part D Donut Hole

The donut hole is confusing – and concerning – enough that it warrants a little more information. Beneficiaries who fall into the coverage gap are often unprepared for the increased expense, so it’s important to take the time to find out if you might enter the gap and what you can expect to pay during this time. Let’s look at the coverage gap in more detail.

You may hear some people say that the donut hole doesn’t exist anymore. That’s simply not true. However, it has gotten better in recent years. In the past, you were responsible for nearly the entire cost of your prescription when you fell into the donut hole. By comparison, today’s coverage gap is much smaller.

We’ve talked about how you get into and out of the donut hole. What we didn’t mention are the costs that are included in your total amount to enter catastrophic coverage. In 2024, you must pay a total of $8,000 for covered prescriptions. (Non-covered prescriptions do not apply to your total amount.)

The out-of-pocket costs considered in the $8,000 include:

- Your deductible

- Your costs during the initial phase of coverage

- Any amounts paid by yourself, family, friends, or charitable organizations

- Amounts paid by State Pharmaceutical Assistance Programs (SPAPs)

Costs not included in that amount include your monthly premiums, what your plan pays, the cost of non-covered drugs, costs obtained outside your plan’s pharmacy network, and generic medication discounts.

Your plan will keep track of how much you’ve spent during the year, and you can find this amount on your monthly statements or Explanation of Benefits (EOBs). If you change plans during the year, any money you have already spent will be applied to the new plan.

If you qualify for Extra Help, the federal program that assists individuals with prescription drug costs, the donut hole does not apply to you.

How to Enroll in Medicare Part D

You should enroll in a Medicare Part D plan as soon as you are eligible – either when you turn 65 or when you lose creditable coverage, whichever comes last. It’s important to enroll in Part D right away to avoid any late-enrollment penalties.

To enroll in a Part D or Medicare Advantage Prescription Drug plan, you must first enroll in both Part A and Part B of Original Medicare. The earliest you can do so is during your Initial Enrollment Period, which is a 7-month window around your 65th birthday.

Choosing a Part D plan might be the hardest part of your Medicare enrollment. You’ll need to compare your current prescription list against all the plans offered in your zip code to find the one that’s right for you. The experts at Bobby Brock Insurance make this process easy.

First, we’ll get a list of your current medications and ask you which pharmacies you like to use. Then, we’ll determine which plan offers you the least costs throughout the year. You may find that many plans cover all your prescriptions, but some will have higher copayments than others. Bobby Brock Insurance will help you choose the plan that saves you the most money on your prescriptions.

Don’t Ignore Medicare’s Annual Election Period

Once you enroll in a Part D or Medicare Advantage plan, you’ll have to keep that plan for the rest of the calendar year. (Unless you qualify for a Special Enrollment Period.) However, you can change your plan during Medicare’s Annual Election Period (AEP).

AEP begins on October 15 and ends on December 7. During this time, you can change your Part D or Medicare Advantage plan. Even if you’re happy with your current plan, it’s important to review your options for the upcoming year.

Since Part C and Part D plans run on annual contracts, there are usually changes to the plan’s premiums, cost-sharing amounts, and even benefits. You may love your plan now, but it might make changes that negatively impact your coverage in the future. Plus, if you have changes in your prescriptions, you should shop around for plans that cover your new prescriptions in the most cost-effective way.

If you’d like to get help paying for your prescription drugs, talk to a licensed Medicare specialist at Bobby Brock Insurance today!