Part D Estimated Costs

Medicare Part D consists of all prescription drug plans within the Medicare program. It’s available to everyone who is enrolled in both parts of Original Medicare (Parts A and B). As with other aspects of Medicare, Part D can be challenging to understand, especially when it comes to costs.

It’s not just the premiums you have to consider – you’ll need to understand the deductibles, coinsurance, and how certain coverage phases work. Estimating your Part D costs is probably the most difficult part of creating a healthcare budget, but we’ll take you through the most important aspects to be aware of today.

Part D Premiums

Your Part D premium is the monthly cost you pay to keep your prescription drug coverage. There is no standard premium for Part D plans. Instead, you’ll have a variety of plans to choose from in your area. Don’t choose the plan based on the premium alone. You’ll need to consider the drug formulary and the out-of-pocket costs, which we’ll discuss later.

While there isn’t a set standard, there is a national average. As of this year (2023), the national average is around $33 per month. Of course, some plans may cost much less, and some will cost much more. Typically, the premium increases with the level of coverage.

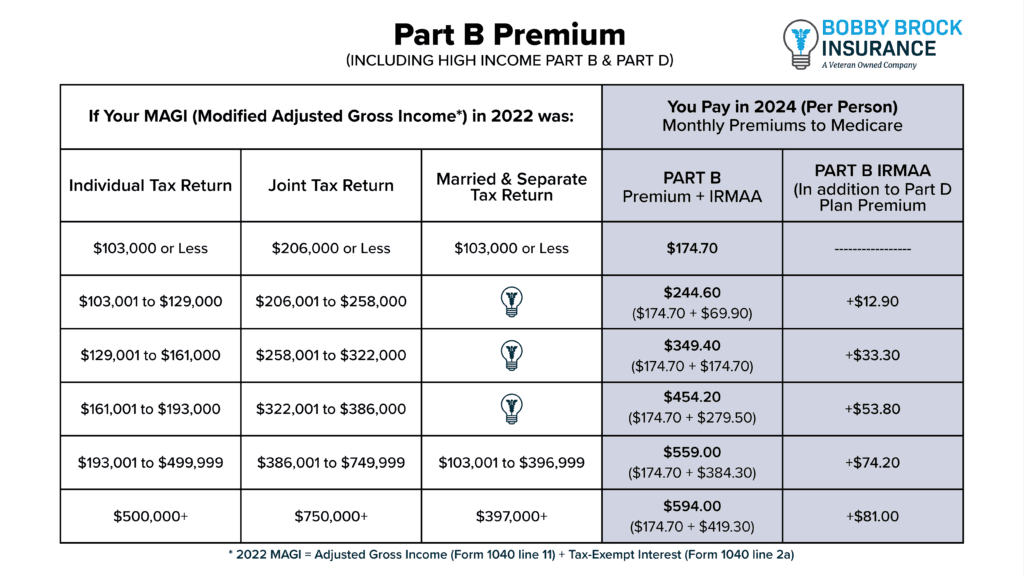

Income-Related Monthly Adjustment Amounts for Part D

Another thing that could impact your Part D premium is your income. IRMAA, the Income-Related Monthly Adjustment Amount, is an additional amount added to your Part B and Part D premiums if your annual income is above a certain threshold.

Social Security will use your adjusted gross income from two years prior to determine if you owe IRMAA. For example, your 2024 IRMAA is based on your 2022 income. IRMAA has several thresholds, each with varying amounts, and these thresholds change each year.

If you owe IRMAA, it will be added to your monthly premium. However, the payment goes to the Medicare program, not the individual insurance carrier you enroll with.

Part D Late Enrollment Penalties

Another thing that could increase your Part D premium is late enrollment penalties. Medicare has several penalties, but by far, the most common is the Part D penalty.

If you do not enroll in Part D as soon as you are eligible, you’ll incur the late enrollment penalty. And yes, unfortunately, you’re penalized even if you don’t take any prescriptions!

The Part D penalty is calculated by multiplying 1% of the national base beneficiary premium ($34.70 in 2024) by the number of months you were eligible for Part D but did not enroll. Round to the nearest $0.10 and tack that number onto your premium.

For example, if you waited 24 months to enroll, your monthly penalty would be $8.10. You pay this penalty for the rest of your life or as long as you have a Part D plan.

Part D Deductibles

As we mentioned earlier, your premium is not the only amount you’ll need to consider when estimating your Part D costs. The next thing we need to look at is the deductible.

A deductible is the amount you must pay out-of-pocket for your prescriptions before the Part D plan begins to pay its share of covered drugs. Each year, the Centers for Medicare and Medicaid Services (CMS) sets a standard deductible. Most plans choose to use the standard deductible, but plans can choose to have lower (but never higher) deductibles. In 2024, the standard Part D deductible is $545.

Plans with lower deductibles may sound appealing, but they may not always be the best choice. Plans with lower deductibles may have higher premiums or other costs, so you’ll have to balance all these aspects. Plus, many plans waive the deductible on drugs that fall within the first one or two tiers of the drug formulary. Many common, generic medications will not apply to the deductible.

Also, note that if you receive Extra Help, a program to help people with limited income and resources pay for prescriptions, your deductible may be lower or even eliminated.

Part D Coinsurance Costs

After you’ve paid your deductible, you’ll enter the initial phase of coverage. During this time, you’ll pay only the coinsurance amount for your prescription. The coinsurance will vary based on your plan and where each medication falls on the drug formulary. Generally, drugs in lower tiers are cheaper than those in higher tiers. Higher tiers are reserved for name-brand and specialty medications, so plan to pay more for these.

The Coverage Gap or Donut Hole

A unique aspect of all Part D plans is the coverage gap, often referred to as the “donut hole.” If you find yourself in the donut hole, you’ll pay a higher coinsurance amount.

Like other numbers we’ve discussed, the amounts needed to get into the donut hole vary each year. In 2024, you enter the coverage gap when you and your plan have spent a total of $5,030 on covered medications. While you’re in the coverage gap, you’ll pay about 25% of the cost of your medications.

Starting January 1, 2024, once your out-of-pocket spending reaches $8,000 (including certain payments made by other people or entities, including Medicare’s Extra Help program, on your behalf), you’ll automatically get “catastrophic coverage.” This means you won’t have to pay a copayment or coinsurance for covered Part D drugs for the rest of the calendar year.

As with the deductible, if you are enrolled in Extra Help, you won’t need to worry about the coverage gap.

Saving Money on Prescription Medications

While Medicare Part D helps alleviate the cost of prescription drugs, it’s wise to explore additional strategies to manage your medication costs effectively. We’ve got a few tips to help you save on prescription medications.

- Use Generic Drugs: Whenever possible, opt for generic versions of your medications. They’re usually placed on lower tiers of the formulary, which means lower coinsurance costs for you. Discuss this option with your doctor or healthcare provider and find out if there are any generic alternatives to your current medications.

- Review Your Plans Annually: Every year, you should review your Medicare plans during the Annual Election Period (October 15 – December 7). It’s important to utilize this time, even if you’re happy with your current plan. Formularies and plan details can (and often do) change from year to year.

- Apply for Extra Help: If you have limited income and resources, you might qualify for Extra Help. This is a federal program run through individual states, so reach out to your state’s Medicaid department to find out if you qualify for either full or partial Extra Help.

- Manufacturer’s Patient Assistance Programs: Many pharmaceutical companies offer assistance programs to people who can’t afford their medications. Check the manufacturer’s website or ask your healthcare provider for information on available assistance programs.

- State Pharmaceutical Assistance Programs (SPAPs): Some states offer help with paying drug plan premiums and other drug costs. Check to see if your state has a program that could assist you.

- Mail-Order Pharmacies: Many Part D plans offer a mail-order pharmacy option. Not only is this convenient but using your plan’s mail-order services often saves you money.

- Prescription Discount Programs: There are a variety of prescription discount programs or clubs. Some examples include Cost Plus Drugs, GoodRx, SingleCare, and Blink Health. Many local pharmacies also have their own savings programs, like Kroger Rx or Walmart’s $4 Prescription Program. These are great options and are sometimes even cheaper than using your Part D plan.

Quickly Estimate Your Part D Costs

This all sounds quite complicated, and it is. However, if you get help from an advisor at Bobby Brock Insurance, we’ll be able to estimate all these costs for you. Our calculators will find the Part D plan that is most cost-effective for you, and we’ll be able to map out your costs over the course of the year.

We’ll know which drugs apply to the deductible, when you might enter the coverage gap, and how much you should budget for the entire year.

Our agents are here to help you find the most affordable option that will give you the most benefits. Give us a call now to compare Part D rates in your area.