Did you know that not everyone pays the same Medicare premiums? The Centers for Medicare and Medicaid Services (CMS) set a standard premium each year, which is what the majority of beneficiaries pay. However, about 8% of people actually pay a higher premium for both Medicare Part B and Medicare Part D.

The higher premium is called IRMAA, the Income-Related Monthly Adjustment Amount. Depending on your income, your Medicare premiums could be increased significantly. Unfortunately, many people don’t realize they’re subject to IRMAA until they get the bill – not the kind of surprise you want!

The good news is there are ways to appeal IRMAA. Today, we’re going to break down IRMAA for Part B and Part D and take you through a step-by-step guide on how to appeal IRMAA if it applies to you. Plus, we’ll teach you how to avoid IRMAA altogether by planning ahead!

How Your Medicare IRMAA Is Calculated

Before we get into the specifics of how to appeal IRMAA, we need to understand how it’s calculated. As the name suggests, IRMAA is income-related. If you earn a high income, you’ll pay more for your Medicare premiums. The reason for the increased amount is to try to create a more balanced Medicare program where those who make more money contribute more to the Medicare trust funds.

To determine if you pay IRMAA, the Social Security Administration (SSA) looks at your Modified Adjusted Gross Income (MAGI) from two years prior. So, for 2023 premiums, they’ll look at your income from 2021. If you filed independently, only your premium is affected. If you filed as a married couple, both of you will be subject to IRMAA if your income allows it. Social Security will notify you of the higher premium amount, along with an explanation of their determination.

2023 IRMAA for Part B and Part D

How much is IRMAA in 2023? Below is a chart of the adjusted premiums based on income thresholds. This year, $164.90 is the standard amount most people pay. Below that, you’ll find the adjusted amounts based on your income and filing status.

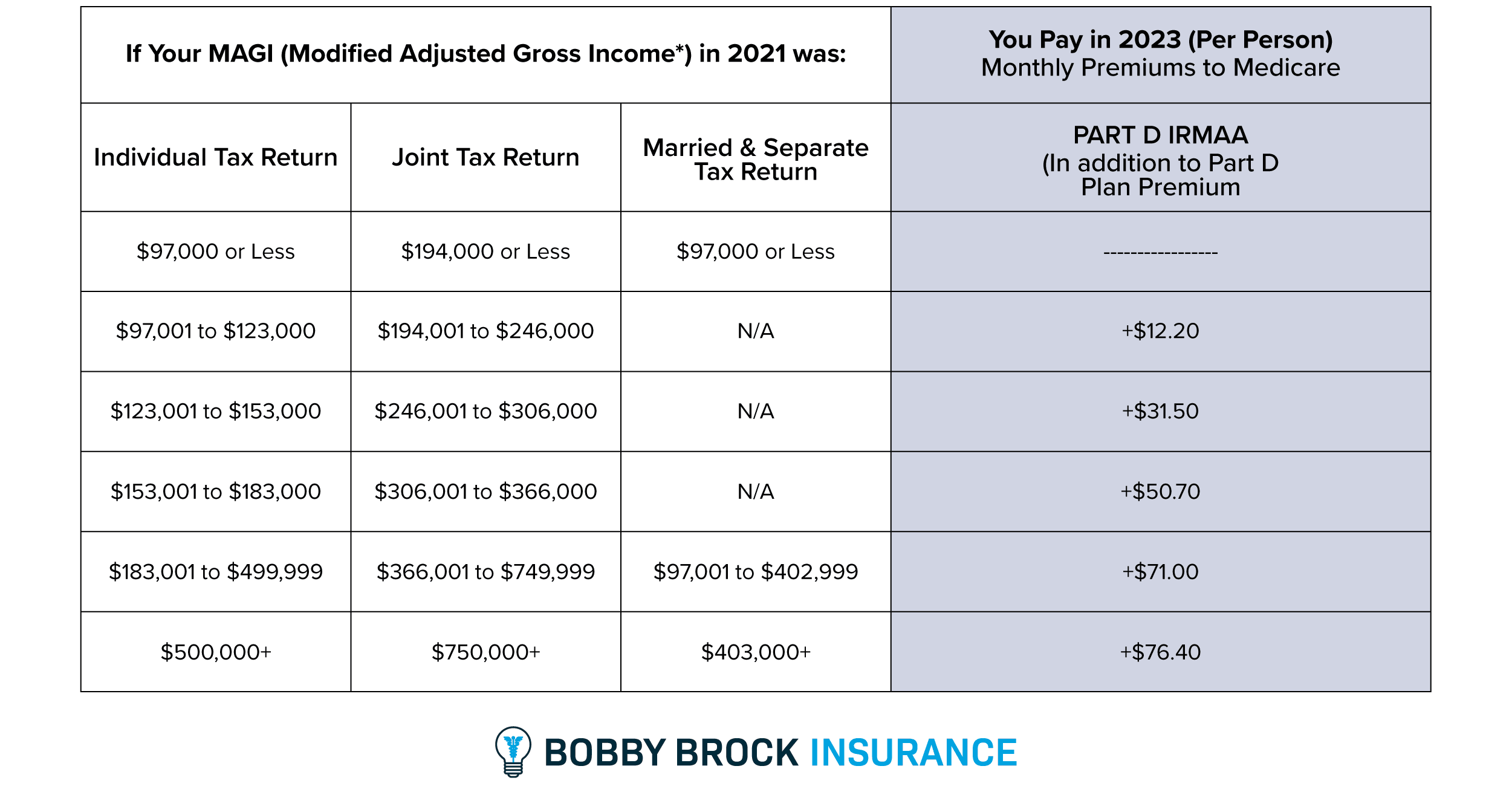

Next, we need to look at IRMAA for Medicare Part D. Fortunately, these adjusted amounts aren’t quite as much as they are for Part B, but they can still have an impact on your healthcare budget, especially if you are already enrolled in a higher-premium Part D plan.

IRMAA for Part D is added to whatever premium you pay for Part D. There is not one standard premium like there is for Part B since there are so many different Part D plans to choose from. Add the Part D IRMAA to your existing plan premium, and you’ll have your total premium. For example, if you are enrolled in a Part D plan that costs $21 per month, and you fall into the highest IRMAA threshold, your premium would be $97.40.

Appealing Your Medicare Part B and Part D Premiums

Since the SSA looks at your income from two years prior, it’s not uncommon for beneficiaries to have had a significant change in their income. This happens most often to new beneficiaries who have recently retired. Their new, fixed income is often less than it was when they were actively working. If you find yourself in this position, you have a great case to appeal IRMAA.

Let’s take a look at a few other reasons you may be qualified to ask for a reconsideration of your Medicare IRMAA.

Qualified Events for Medicare Premium Appeals

Qualifying events are often big, life-changing events that have impacted your income. A few other reasons you may consider an IRMAA appeal include the following:

- Marriage, divorce, or the death of a spouse

- Changes or termination of a pension

- Losing an income-producing property

- Receiving a settlement from an employer due to company bankruptcy or closure

You can also appeal your Medicare IRMAA if you feel the MAGI on your tax return is incorrect. However, this is a situation that will require a bit more work as you’ll have to contact the IRS to correct the information prior to beginning the appeal process.

How to File Your Appeal

Think you might qualify for an IRMAA appeal? Great! Let’s walk through the steps you’ll need to take to file your reconsideration request.

Step 1: Print Form SSA-44: Medicare Income-Related Monthly Adjustment Amount-Life-Changing Event. This form will walk you through the entire appeal process and list the documentation you’ll need in order to file the request. Documentation may include evidence of a drastic change in MAGI or of a life-changing event, like a marriage certificate.

Step 2: Fill out the form and attach copies of all the required documentation. Provide as many official documents as you can to support your case. You may also want to write a cover letter that further explains your situation. When you are finished filling out the form, add your signature. It’s a good idea to keep a copy of your request in case the original is lost.

Step 3: Submit your appeal. You may submit your appeal by fax or by dropping it at your local Social Security office.

You will continue to pay IRMAA while your appeal is processing. However, if your appeal does get approved, you may be reimbursed for the months you overpaid. In most cases, they apply the overpayment as a credit towards future premiums.

Not every appeal is approved. If you received an inheritance one year or got lucky at the casino, it’s unlikely Social Security will grant your reconsideration request. Unfortunately, you’ll have to pay the higher premiums for a year. Remember, IRMAA is re-assessed every year, so if you have a sudden change in income, you aren’t stuck paying IRMAA forever!

There is no harm in filing an appeal if you think you may be eligible to lower your Medicare premium. The form is fairly short, so it’s certainly worth your time and effort to try!

How to Avoid IRMAA

Planning your retirement a few years early is the best way to save money on your Medicare premiums and avoid IRMAA altogether. Medicare premiums and IRMAA thresholds typically change every year, but they should give you an idea of what to expect if your retirement date is just a few years down the road.

Are you someone who might fall into a higher IRMAA bracket? You should start working with your financial advisor and outline a strategy to minimize your Medicare premiums. Talk to them about when you plan to retire, and then organize your retirement distributions to reduce the risk of paying IMRAA if possible.

Other Ways to Minimize Healthcare Costs

Whether you’re stuck paying IRMAA or not, you’ll need to take some time to look for other ways to save on your healthcare costs.

Medicare Supplement Plans

Medicare Supplements, also known as Medigap plans, are secondary insurance plans that pick up the majority of your healthcare costs. After Parts A and B pay their share, your Medicare Supplement plan will pick up some or all of the leftover expenses. While these plans do have an additional premium, they will save you thousands of dollars in cost-sharing when you need to use them.

Plans F, G, and N are all popular choices among our clients. Premiums vary based on your age, gender, location, and tobacco use. Our agents are happy to explain what these plans cover and provide you with quotes for all three.

Medicare Advantage Plans

Medicare Advantage plans, also known as Medicare Part C, are another great way to save money on your healthcare. Most Part C plans have very low premiums – some are even as low as $0 per month! You’ll still have some copays under these plans, but they offer additional benefits you won’t find in Original Medicare or a Medicare Supplement plan. Instead of having multiple policies to cover all your needs, Medicare Advantage plans are an all-in-one alternative that simplifies your benefits.

If you’d like more information about Medicare premiums and how IRMAA works, contact the experts at Bobby Brock Insurance! Our agents can review plans you already have in place and help you find ways to save money on your healthcare. Call us today for your complimentary consultation.

Related Blog Posts

-

Currently, the 2021 Medicare Part B premium is $148.50. That is the amount that most people pay for their Part…

-

2022 Medicare premium and cost sharing increase information has been officially released, and the picture is not as pretty as…